The short- and long-run economic impacts of Hurricane Katrina: some implications for COVID-19

COVID-19 has created a public health crisis. The measures taken to slow its spread are also grinding a lot of economic activity down to a halt and making an unprecedented number of workers unemployed, which will likely bring about a severe recession. Insights from past recessions – such as the financial crisis of 2008 – will undoubtedly be useful for addressing the economic impacts of COVID-19. However, there is another large, sudden, external shock to (parts of) the US economy that, like COVID-19, was not caused by overvalued housing markets, excessive leverage, or a sudden drop in consumer confidence. The event was Hurricane Katrina, which devastated the city of New Orleans and parts of the Gulf Coast in 2005. I have studied Hurricane Katrina extensively in my research, and there are some important lessons we can learn from the natural disaster.

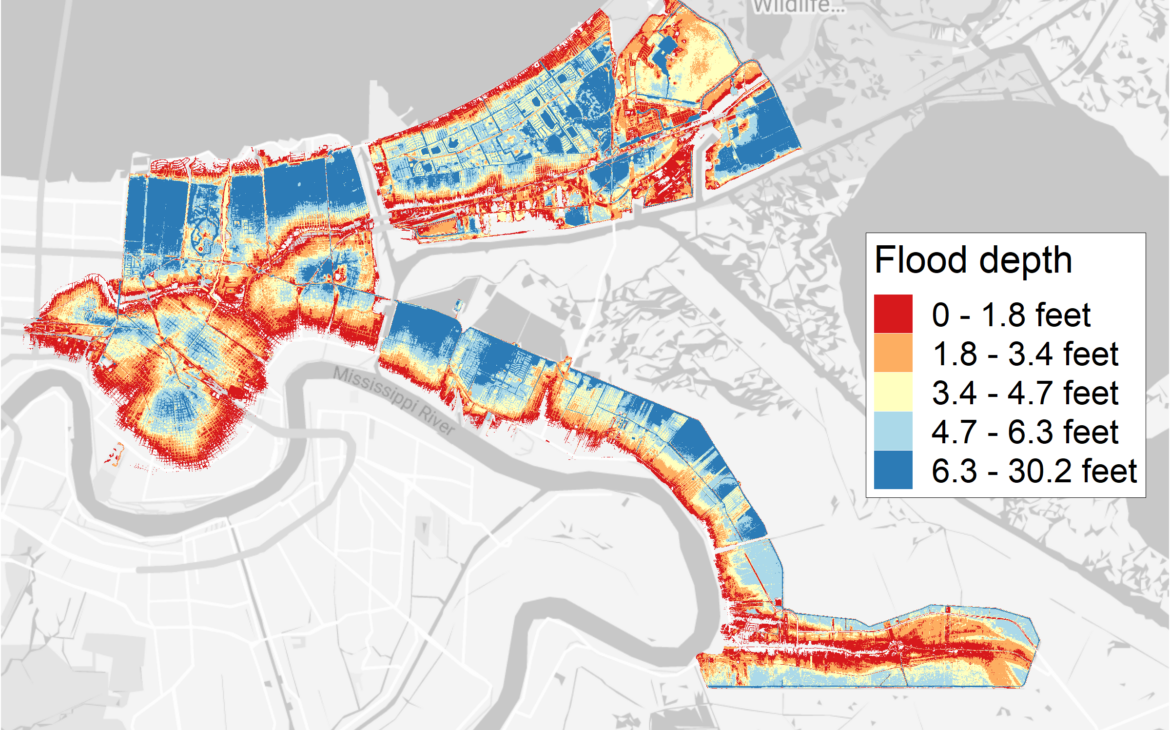

Hurricane Katrina made landfall in New Orleans on August 29, 2005. The storm surge caused widespread levee failures, which in turn flooded 80 percent of the city. In many parts of New Orleans, the flood depth exceeded 6 feet (see map below). Nearly 2,000 people were killed across the Gulf Coast, resulting in a natural disaster death toll that has not been seen in the US since the 1928 Okeechobee Hurricane. Most of the victims were elderly.

New Orleans essentially shut down in the aftermath of Hurricane Katrina. Hospitals closed and so did schools, most of which were destroyed by the storm. FEMA deemed most of the city uninhabitable for months. There were widespread and long-lasting business closures. Many New Orleans residents were laid off, including city workers. Across the Gulf region, an estimated 230,000 jobs were lost. The economic damage to the area was catastrophic.

A few years ago, Laura Kawano, Steven Levitt, and I used tax return data to study the short- and long-run economic impacts of Hurricane Katrina on those who lived in New Orleans prior to the hurricane.* We tracked all households who filed from a New Orleans address in early 2005 regardless of where they moved, studying how they fared economically in 2005-2013.

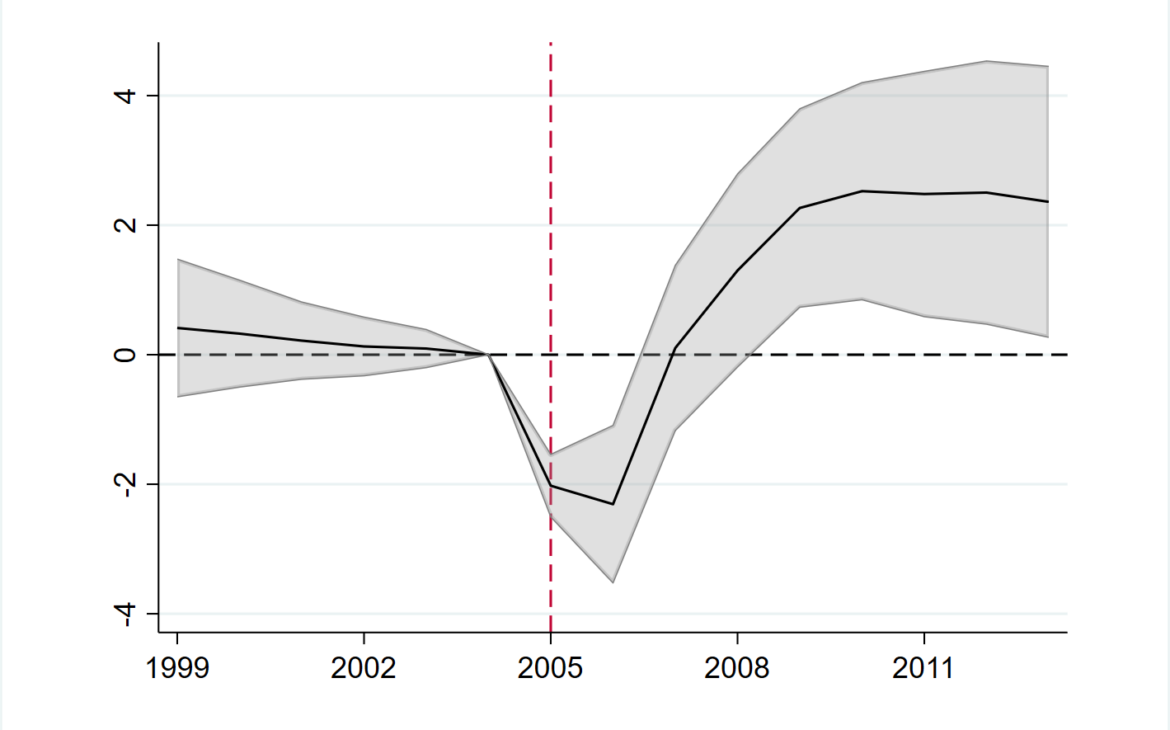

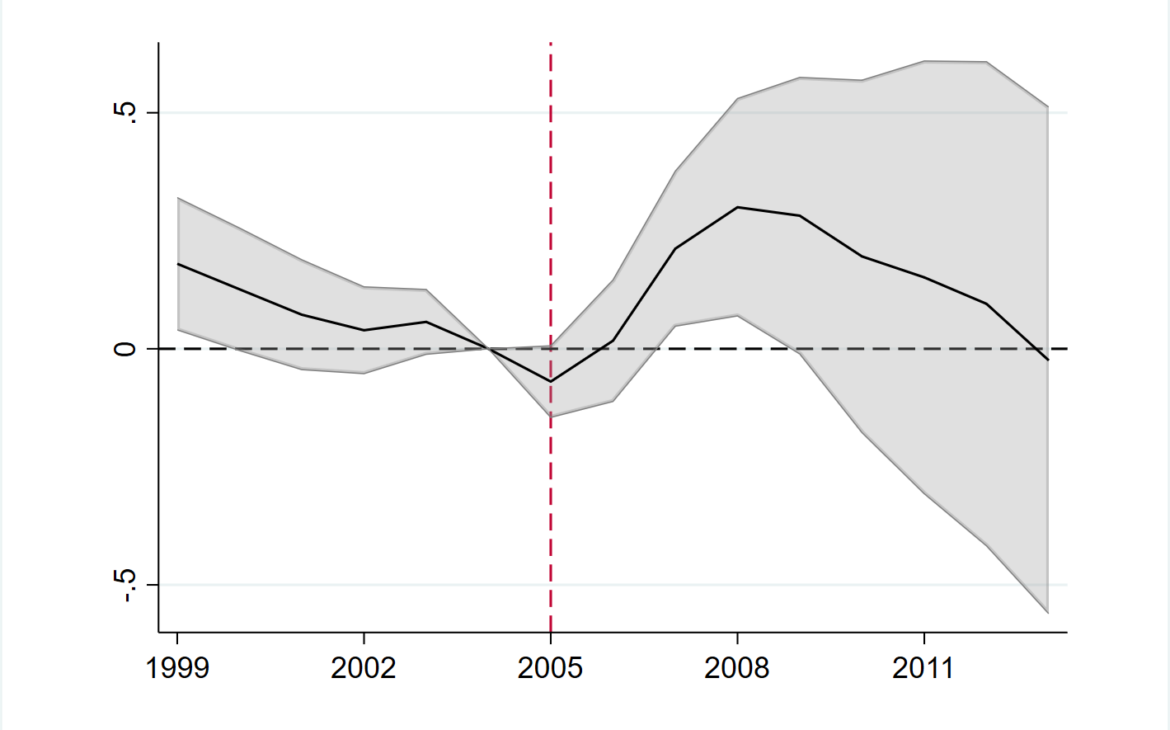

The graph below shows what happened to these households’ labor incomes in 2005-2013, relative to a control group of households living in ten other, unaffected, cities. The vertical red line is the year of Hurricane Katrina, and the estimated income changes (black line) are in thousands of 2005 dollars.

In 2005-2006, average annual labor incomes fell by $2,000-$2,300. That’s a big chunk of the average ($33,000/year in our sample). Thus, Hurricane Katrina resulted in something like 1.5 years of depressed incomes for the average New Orleans resident. Given that Hurricane Katrina struck at the end of summer 2005, the $2,000 average drop in 2005 earnings implies that many households spent the rest of that year with little or no additional earnings. The share of households reporting no labor income in 2006 rose by 4.2 percentage points, a huge increase relative to the average (13 percent). The increase in the number of income-less households implies that the average income drop is driven by a smaller subset of individuals who lost most or all of their income.

Unfortunately, I think a picture like this is also a likely outcome with COVID-19. Unless the restrictions are lifted very soon, people who lost their jobs are unlikely to immediately find a new one that pays the same amount of money. More generally, the economy will take some time to get going again. Thus, income decreases will persist beyond the immediate lockdown period, perhaps for as long as a few years. The longer the restrictions are in place, the longer the post-restriction drop in incomes will last. (Note that I am not saying that we should lift the restrictions and let the virus spread; my goal is only to describe what will likely happen on the economic impact side.)

Now here’s the good news: incomes recovered by 2007-2008. In our sample, incomes ultimately increase to above their pre-Katrina levels, but I think that finding is specific to our study and is unlikely to materialize with COVID-19. Some groups recovered more slowly than others, but we didn’t find any subgroup for whom incomes didn’t return to at least their pre-Katrina levels. If Hurricane Katrina didn’t produce a scarring effect, I doubt that COVID-19 will either. We can never rule out some fundamental shift, like people losing faith in government or major social unrest breaking out. But the reason we’re in our current situation is not because of a fundamental flaw in the US economy. To a first approximation, COVID-19 shouldn’t make anyone’s human capital less valuable in the long run. Of course, a big difference between Hurricane Katrina and COVID-19 is that Katrina victims could immediately move to unaffected areas, which likely made it easier to find jobs. On the other hand, because COVID-19 is not destroying physical capital, recovery may be quicker than with Katrina. Additionally, Hurricane Katrina victims had to move, while COVID-19 shouldn’t make any areas much less economically viable, at least in expectation.

But enough talk about the long run because in the long run we are all dead. Let’s talk about what was done in response to Hurricane Katrina and what’s likely to be helpful with COVID-19.

First, restrictions on who could qualify for unemployment insurance payments were loosened and eligibility review controls were temporarily eliminated (to facilitate quick receipt of payments). A standing Disaster Unemployment Assistance program to help those who can’t work because of a major disaster was also activated (as is standard for any major disaster).

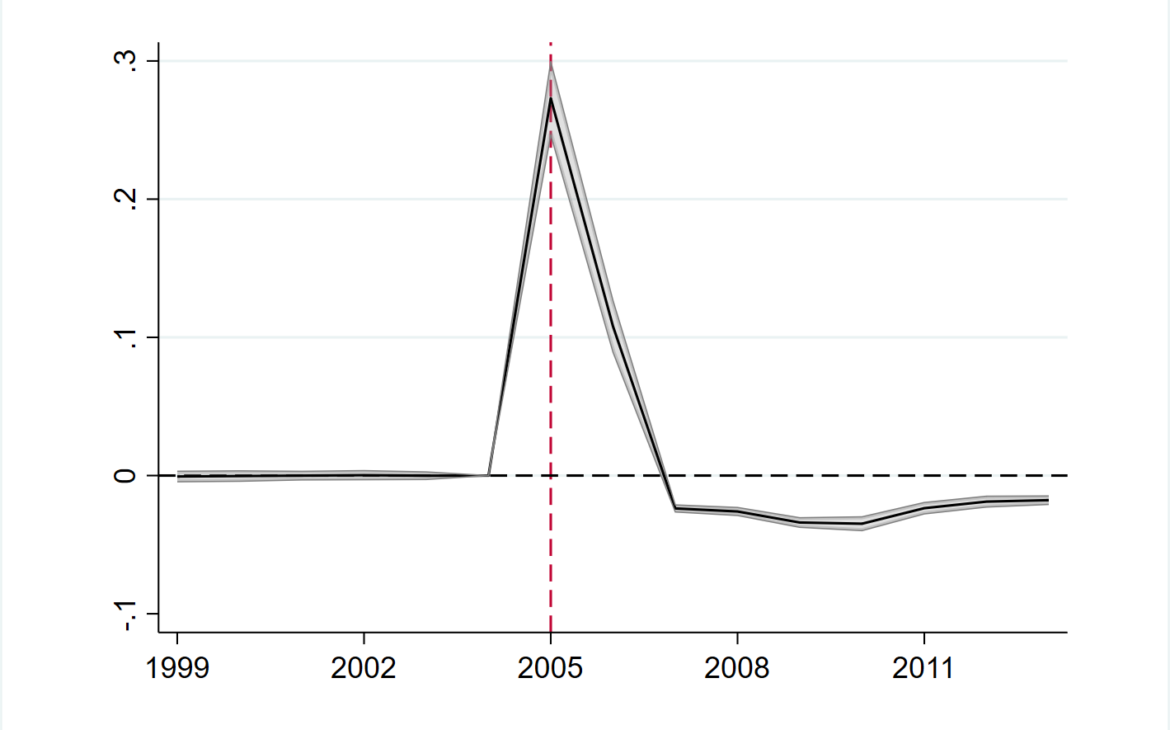

Among the victims we tracked, the share of people receiving any unemployment insurance (UI) benefits increased by over 27 percentage points in 2005, over a mean of 7.5 percent. That is, UI receipt more than quadrupled. In 2006, the probability of receiving unemployment insurance benefits was more than double relative to normal times. Note that unemployment receipt did not fully offset the income losses: when we looked at victims’ adjusted gross income (AGI), we saw a pattern that is qualitatively similar to labor income. Consistent with this, some have argued that the post-Katrina income replacement rates were too low, and I think it would make sense to increase UI generosity during the downturn created by COVID-19.

Individuals living in the disaster area could also withdraw up to $100,000 from their retirement accounts without paying an early withdrawal penalty and could spread the tax payments on those withdrawals over three years. Given that many Americans already don’t have adequate retirement savings, this may not be a good first option, but temporarily eliminating the early withdrawal penalty is still a good idea to give additional flexibility to people who fall through the cracks of whatever system we put into place.

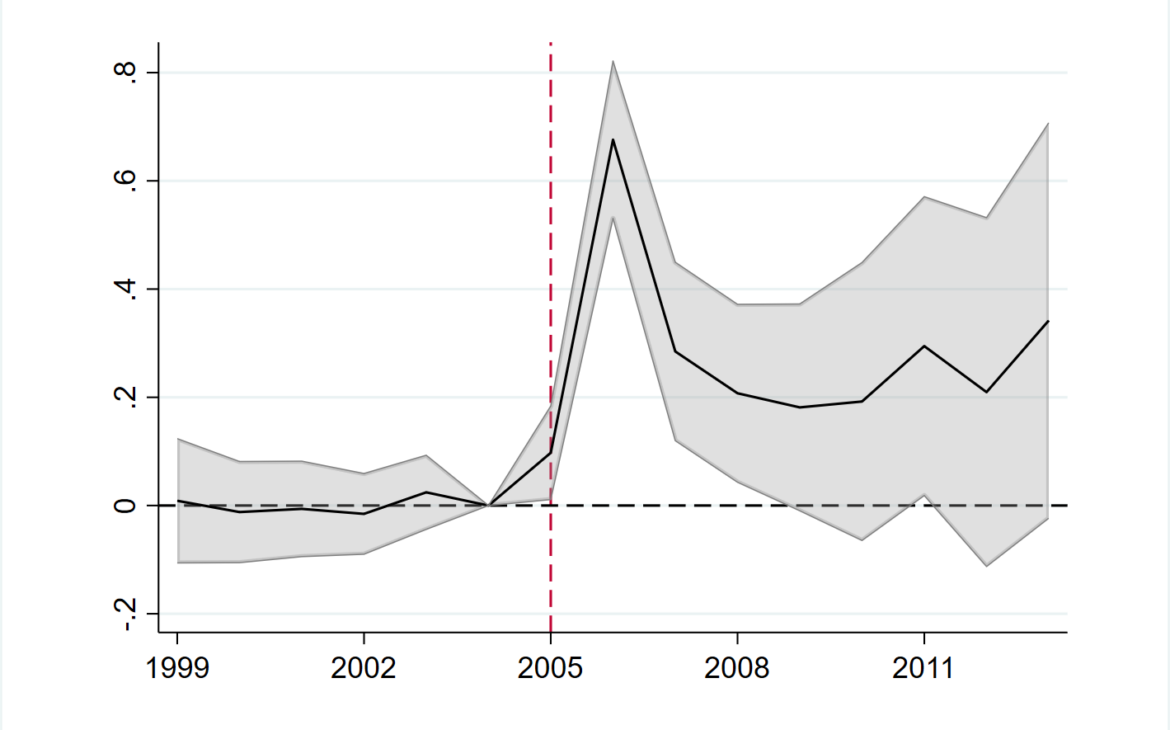

Indeed, the average New Orleans household took advantage of the ability to tap into their retirement accounts. In 2006, the average withdrawal was over $600 and a smaller increase persisted through 2013. (The average masks a lot of heterogeneity: withdrawals were concentrated among the older individuals and among those living in the worst-affected parts of the city.)

Finally, some of the economic effects of Hurricane Katrina manifested themselves in other social safety net programs. Social Security Disability Insurance receipt (SSDI) increased temporarily but substantially. Although our estimates are somewhat imprecise, they suggest that SSDI receipt increased by nearly 30 percentage points in 2008-2009 before declining in the remainder of the study period. Because people typically do not leave SSDI after enrolling, this pattern suggests that Hurricane Katrina caused individuals who would have eventually ended up receiving SSDI to enroll sooner.

These are the key findings of our paper. Emek Basker and Javier Miranda have another important study on business survival in the aftermath of Hurricane Katrina. They find that businesses sustaining physical damage had very low survival rates. Among surviving businesses, recovery was weaker for smaller businesses, with suggestive evidence that financial constraints played a role in this. While there is of course no physical damage to businesses when it comes to COVID-19, the importance of financial constraints in the context of Hurricane Katrina suggests that we may see inefficient business exit following the COVID-19 lockdown as well.

With these findings in mind, here are the takeaways as I see them. If we want to avoid income losses, widespread business closures, drawing down of retirement savings, and a push of people into SSDI, the government will have to be more aggressive than it was in response to Katrina. What might such an aggressive response look like? A statement signed by over 800 economists summarizes it quite well. Here’s a brief summary of the necessary components of the response:

- Invest money into shortening the duration of the lockdown (testing/vaccines/treatments, etc)

- Provide financial and other assistance to help small and medium businesses stay in business

- Provide financial and other assistance to individuals whose incomes are affected by the lockdown

- Support the functioning of financial markets so that large businesses are not threatened

The full text of the statement has additional details on what each policy bundle would entail, and there are many capable economists that can help work the details out further in specific legislation to ensure that the response is sufficient and well-designed.

I believe that implementing all of these policy bundles will minimize the economic impact of COVID-19. Some of these suggestions appear to be in a bill soon-to-be-passed by Congress. But the plan to send most US households checks that only depend on their pre-COVID-19 income is both unnecessarily expensive and not sufficiently targeted to help the worst affected. Giving money to people who are still receiving their full salaries isn’t helpful during a lockdown; this tactic should be reserved for the future, if necessary. The government made many mistakes when it came to the Hurricane Katrina response, and it has also made many mistakes responding to this pandemic. However, unlike Hurricane Katrina, COVID-19 is far from over. Whether our government will ultimately do better this time around remains to be seen.

* The paper is now published in American Economic Journal: Applied Economics (ungated version here). Jeff Groen, Mark Kutzbach, and Anna Polivka did a concurrent analysis of post-Katrina earnings dynamics (using a different control group) and came to similar conclusions.

Comments are closed.